Hard Hitting Conservative Commentary by Gary M. Polland

Volume XXIII Number 8 – June 3, 2024

Thoughts This Fortnight

Proof That Your Vote Counts

Runoff Contests Settled by a Handful of Votes

By Marc Cowart, Managing Editor

Some of Tuesday’s primary runoff elections were decided by the slimmest of margins, proving once again that every vote counts, especially in low turnout elections. The Republican Primary Election for Congressional District 7 for example was decided by a razor-thin margin of just 42 votes. In that CD-7 contest, of the 418,014 registered voters, a scant 5006 participated. That’s a paltry 1.2% turnout. Granted, that seat is currently held by a Democrat and the Republican is a long shot, but that’s all the more reason to turn out in force and show the Democrats that Republicans are energized and won’t go down without a fight. 5006 votes don’t exactly send that message.

In the high-profile slugfest where Speaker of the House Dade Phelan was fighting to protect his seat, the margin of victory was just 366 votes out of 125,633 votes cast. Despite millions of dollars spent to persuade and turn out votes, just 20.11% of registered voters turned out for that race. The takeaway here is that every vote counts. If you skipped the runoff election and your candidate lost, shame on you.

Don’t Miss Another Chance to Vote

Just a reminder that there is one more chance to vote—in the runoff election for Harris County Appraisal District (HCAD) Board of Directors. TCR has two endorsed candidates in that race: Kyle Scott who is running for HCAD, Director, At-Large, Place 2, and Ericka McCutcheon for HCAD, Director, At-Large, Place 3. TCR urges conservatives to get out and vote for these endorsed conservative candidates who can make a huge difference on this taxing entity. Early voting runs June 3-11 with Election Day on June 15. Polling locations can be found at https://www.harrisvotes.com/Vote-Centers.

TCR – THOUGHTS THIS FORTNIGHT

By Gary Polland, Publisher and Editor-in-Chief

- What is going on with illegals in the country attempting to gain entry to our military bases? It has happened over 100 times. The “mainstream” media gives it scant coverage. Is this preparation for an invasion, terrorism or worse? With open borders, you do not have a country.

- This one is really depressing. According to the Washington Free Beacon, more than 50% of recent UCLA med-students failed their standardized tests after their clinical rotation. One professor commented regarding the outrageous fail rate (hello DEI) is “as bad as you could possibly imagine.” Think about this next time you encounter a young doctor. Whatever happened to the best and brightest getting admitted to medical school? The radical left destroys whatever it infects.

- Trump’s Bogus Trial – It has mercifully ended. TCR is still trying to figure out what he is on trial for.

OUTRAGES OF THE WEEK

- The International Criminal Court (ICC), which neither the U.S. nor Israel is a member, announced it was seeking arrest warrants for Israel leaders and some Hamas leaders. First, there is no moral equivalency between Israel and Hamas. Second, the casualty figures are the lowest relative to soldiers in modern war history at around one to one! War is tough, but Israel has taken extraordinary precautions. Do not be confused, Hamas wants to eliminate Israel. They have a one-state solution in mind that is judenrein (no jews) in Israel. Remember the American and Israeli hostages they are still being held assuming g they are still alive.

- The Biden administration’s unconstitutional forgiveness of student loan debt is now up to costing $167 billion (of course more “borrowed” money and increasing the record of deficit which fuels inflation). This illegal transfer goes from the working class to the upper classes. The message it says to citizens who paid back their student loans is “you were a sucker.”

ARE WE BACK TO THE EVERYTHING BUBBLE?

By Contributing Editor and economist Neland Nobel and

reprinted from The Prickly Pear newsletter a sister publication to TCR

The term everything bubble was coined when seemingly all investments started to rise in unison, apparently in response to massive liquidity injected into the economy by both the Federal Reserve (monetary policy) and massive Federal deficit spending (fiscal policy). Many also believed that the force pushing all asset prices up at the same time was the era of zero interest rates.

While the inflation of asset prices has continued, it seemed to take some time before the price level of everyday purchases started to rise sharply. Some have suggested this had to do with macro factors such as globalization and demographics. Whatever it was, there was a surprising delay but in the past few years, consumer price inflation has hit with full force.

A rise in asset prices is especially enjoyed by those wealthy enough to own stocks, bonds, real estate, gold, commodities, and cryptocurrencies. This has helped magnify the wealth gap between the ultra-rich and the rest of us.

The only markets not participating of late are the bond market, locked in a four-year bear market, the worst in history, and sectors of commercial real estate. Everything else seems to be floating higher pretty much together once again.

But since most people are not that wealthy, and may own either a limited amount or no assets at all, the sharp rise in consumer prices has caused a political firestorm. Wages have risen much slower than either the cost of consumer items or the cost of credit.

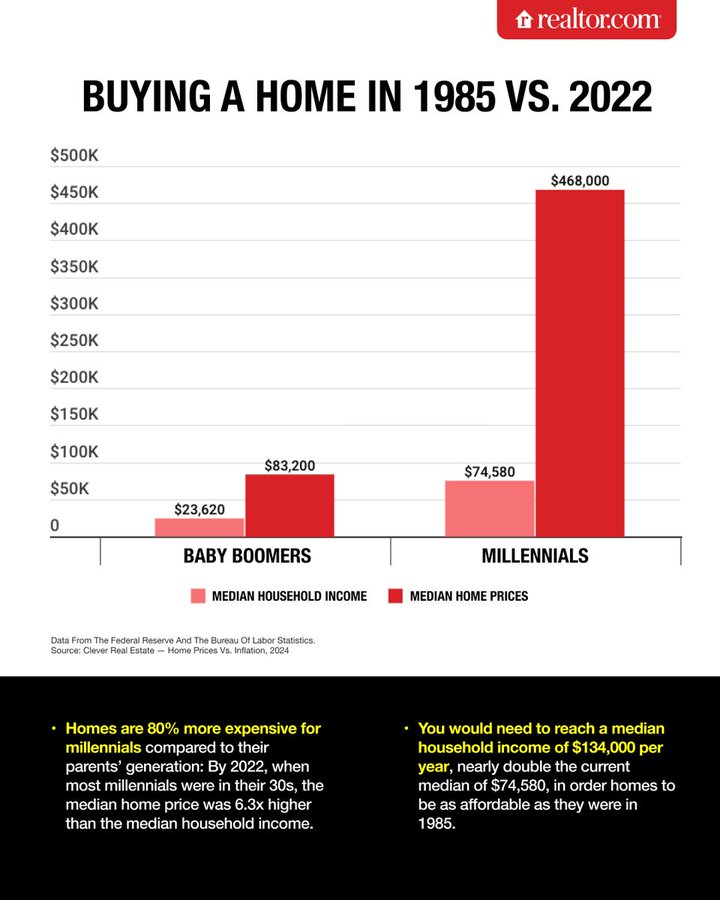

Housing affordability is at the worst level ever recorded. That puts home ownership out of reach for many younger people.

This may explain why we have seen a political switch of historical dimension. The Democrats have become the party of the ultra-rich asset owners and the Republicans have become a working-class party.

The Federal Reserve responded to the bottom-up political pressure of consumer inflation by initiating the sharpest rise in interest rates in percentage terms in American history. This is because the rate of change from zero to even modest levels of 4% or 5% is a tremendous difference, even though nominal rates are not as high as we saw in the early 1980s. While the hike in rates has tanked the bond market and made housing less affordable, the overall economy has seemingly dodged the recession call.

Besides rates, the FED reversed course on asset purchases for their balance sheet. After years of Quantitative Easing (buying bonds to be held by the FED with money created out of thin air), they have been forced to “tighten” by selling those bonds (Quantitative Tightening.)

Most markets went into a downward corrective phase, but as we wrote last time, few seem to violate anything more than short-term trendlines and moving averages.

But, in the past few weeks, stocks, gold, and commodities are back to their rising trajectory, with many going to new highs. That seems illogical given the market views the FED action as “tightening” money and credit.

So, as the FED increased interest rates and shrank its balance sheet, measures of liquidity (how much money is sloshing around the financial system) were rising again. If that seems contradictory, maybe it is because it is.

With markets going to new highs ,the equity market remains overvalued by almost any metric. And, the economy is not growing nearly as fast as asset markets are escalating. This seems very odd for what has been called “tightening.”

For us, the big question is: How can the “everything bubble” come back if the Fed is tightening money?

This has caused quite a debate among analysts, and we have to admit, that we have found it hard to understand ourselves.

The easiest explanation is that while rates are higher, the FED IS NOT TIGHTENING.

How can that be?

As we pointed out last time, both the Bloomberg Index of Financial Conditions and the Chicago Federal Reserve’s Index of Financial Conditions, both show that monetary conditions are easing and not tightening. In addition, the money supply after contracting somewhat, is back to expanding.

In short, money is not tight although it may be more expensive. That distinction is important.

The reason we think that is the case is that fiscal policy remains very loose, and indeed some estimate only about 17% of the huge stimulus from the CHIPS ACT and the Infrastructure Bill, has even been spent. There are trillions in the pipeline yet to squander.

The other explanation is the FED, like any good magician, has you looking at one thing while doing another. It has raised rates, but it also quietly retreated on the rate of QT balance sheet reductions. Secondly, the FED employs a dizzying array of liquidity facilities that few know much about.

Most investors understand if interest rates go up, it will tend to reduce money and credit. However, the FED has many new tools that only someone with a doctorate in financial plumbing can truly understand.

Here are just a few of these other liquidity facilities the FED and Treasury can employ:

- Term Auction Facility or (TAF)

- Primary Dealer Credit Facility (PDCF)

- Commercial Paper Funding Facility (CPFF)

- Term Asset-Backed Securities Loan Facility (TALF)

- Money Market Mutual Fund Liquidity Facility (MMLF)

- Municipal Liquidity Facility (MLF)

- Exchange Stabilization Fund (ESF)

- Supplemental Financing Program (SFP)

- Capital Purchase Program (CPP)

- Paycheck Protection Program (PPLF)

- Treasury General Account (TGA)

- Reverse Repurchase Agreement Facility (RRP)

- Bank Term Funding Program (BTFB). This last one JP Morgan says put $2 Trillion into the pot although they quit lending after March 11, 2024.

Have your eyes glazed over yet? In researching this issue, we are not sure this is even a complete list and likely more will be invented when they want to use them. The main takeaway is that there are many sources of liquidity beyond the discount window.

The bottom line is this: the employment of all these liquidity facilities has more than offset the money being taken out of the system through interest rate hikes and QT.

If that is true, markets ranging from stocks to copper are likely unlikely to take any significant correction, at least for a while longer. Of course, the state of liquidity will have to be monitored because while the FED and Treasury can provide credit, they can’t force people to utilize that credit.

For example, banks create money as well through the lending process. But if consumers and businesses don’t want to borrow at these rates, or economic conditions are too soft to warrant borrowing for expansion, money will not get created by banks, and banks in turn don’t need help from the FED. The term of the art is “pushing on a string.”

To be sure, watching all these liquidity facilities, and how they may interact with each other, is a full-time job. For those in a position to do so, many concede the point we are attempting to make. That is, the FED has increased rates and has been slow at lowering them, but that does not mean liquidity is not plentiful enough to drive markets higher.

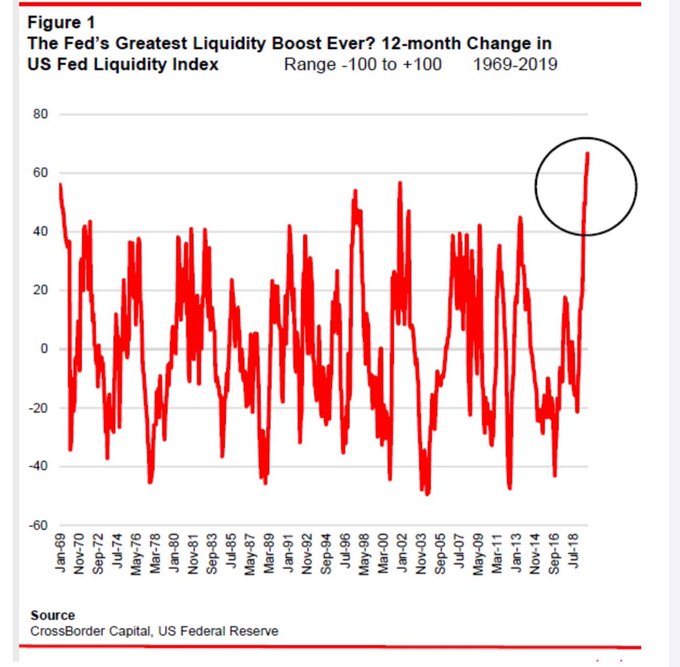

Liz Ann Sonders, Managing Director and Chief Investment Strategist at Charles Schwab, recently commented on this chart.

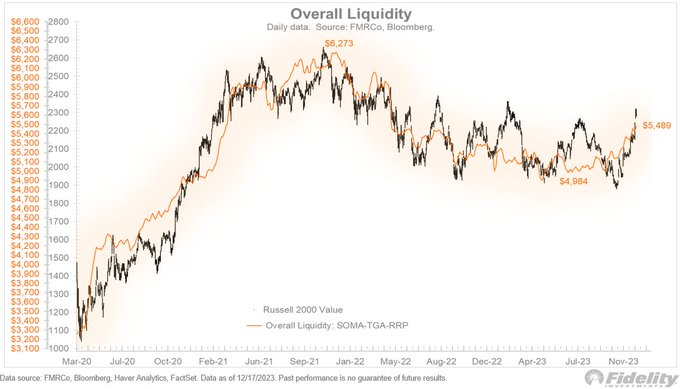

She suggests these multitudinous credit facilities have created one the greatest spikes ever in liquidity in the past 50 years, despite the common belief the “FED is tightening.” Jurien Timmer is a top analyst with Fidelity. He shows that liquidity was contracting, but he too shows it is now expanding. His chart also indicates a close relationship between liquidity and the direction of stock prices. That is likely more than correlation. When money is plentiful, Wall Street has ingenious ways to use it with leverage.

Where all this will end is worrisome. Government manipulation of credit by the FED, or its new-fangled “facilities,” is blamed by Austrian Theory economists for causing both economic and market booms and busts. We think they have a point. If they are correct, it does not matter if excess liquidity comes from traditional sources or a new alphabet soup of credit facilities. It still creates malinvestment, currency debasement, and the destruction of the middle class. It is all artificial stimulation with printed money, albeit in a new format.

So regardless of the mechanism, currency inflation causes both asset and consumer price inflation.

So the good news is, the FED has not been nearly as tight as most of us thought, and that has supported markets and kept them from correcting.

The bad news is, the overvaluation of markets is because the FED is not really tightening, the excesses are not being wrung out of the markets, and consumer price inflation will be harder to subdue. Because of the latter, that means interest rates are likely to stay ‘higher for longer.”

Monetary economist also point out that simply a reduction in the rate of money printing will cause an economy addicted to inflation to go into withdrawal. In short, the elevated levels of many markets is because the fiscal and monetary authorities are not really serious yet about killing off inflation.

That could set us up for a super cycle of unusual magnitude. Markets will eventually correct, albeit from even more extreme levels.

To be sure the FED is very clever with all their credit facilities but it is not clear continuing to blow up serial bubbles in a variety of markets is longer term a good thing.

All these new sources of liquidity certainly complicate matters in figuring out exactly what the FED is doing, and it should be clear to the reader that things are more complex than just following press reports that the FED is tight with money.

The cost of money is one thing, but the supply of money is another. In summary, pay less attention to what the FED is saying and more attention to what they are doing.

A Sad Day for Our Justice System

By Brian Ettinger

The verdict is in on the Trump trial marking a sad day for our judicial system. The State of New York brought this case based on the actions of President Trump before he was President. The Jury verdict based on evidence and Judge rulings was tainted because of the Judge’s handling of this case. New York was once a premiere legal justice system.

When I was in law school, they referred to New York law and Judge Benjamin Cardona and cases he decided as setting precedent for our legal system. To use the New York judicial system for political purposes is setting a bad precedent. President Trump’s conduct led to this case, the verdict and other cases he is defending, but there is no justification to deny him his due process rights and violating his First, Sixth and Seventh Amendment rights under our Constitution.

Judge Juan Marchin is no legal genius and how he handled this trial will lead to other political trials. This Judge opened the flood gates to other State District Attorneys to bring charges against Federal elected officials of opposing political parties and no state has the right to enforce Federal Law violations or charges.

So, a sad day for our justice system. It does not matter if you support President Trump or not, but the weaponization of the justice system will lead to the destruction of both our political and justice systems. Just my two cents.